Good Month-End Close Process Ensures Strong Decision Making

Review Every Account

Key Takeaways:

- Make sure every transaction is reviewed and reconciled to get a clear picture of your company’s finances.

- Properly categorize expenses and capitalize long-term assets to avoid skewed monthly statements.

- Stay on top of outdated AR and AP to protect cash flow and maintain healthy vendor and customer relationships.

Having full, accurate information about the financial health of your business is critical to good decision making. Whether you are looking to buy new equipment, hire employees or seek an increase in your line of credit, using real time data that accurately tells the story of your balance sheet, profit and loss statement and cash position will guide you in making the right decisions. And if your company is in growth mode, discussing a merger or experiencing a financial crisis, the integrity of your financial data is even more important.

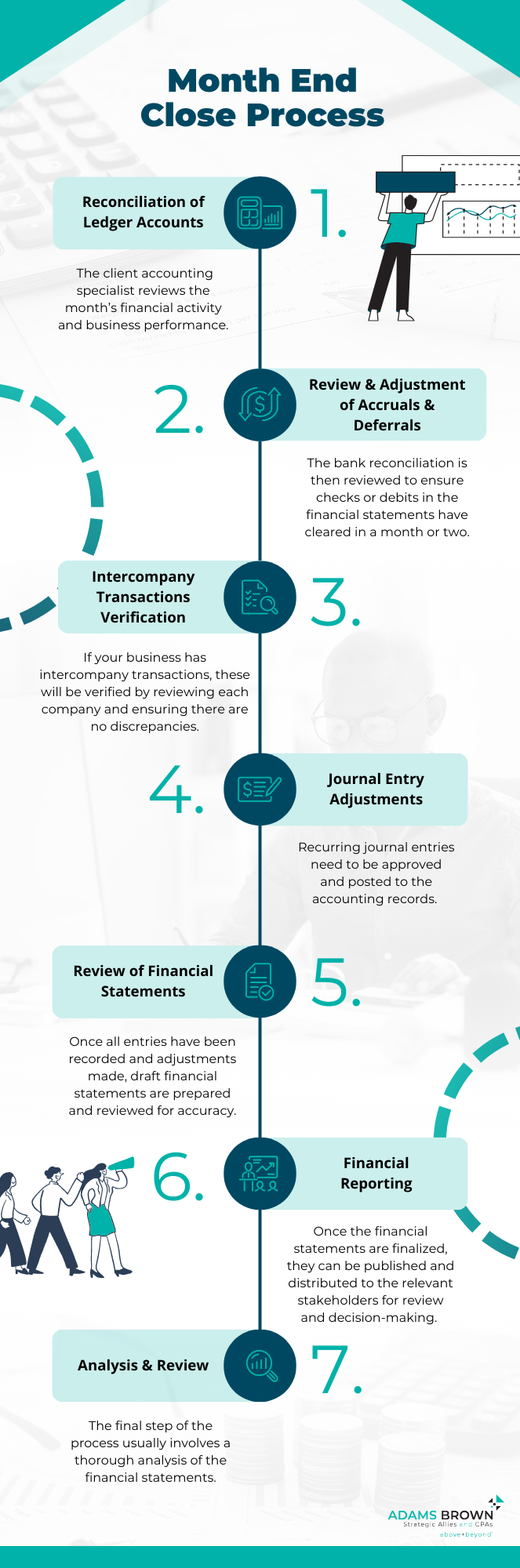

One of the keys to making sure you have complete and accurate data is a strong month-end close process.

Many business owners mistakenly believe the month-end close is just making sure the balance sheet is balanced, expenses are posted, and the P & L matches the balance sheet. But it is so much more.

Review Every Account

First, every account – and every transaction within each account – should be looked at. Reconciliations for cash transactions and credit card transactions, comparing bank to book records, must be prepared. Consequently, good third-party records such as bank statements and merchant account statements are essential to the month-end close process. If you utilize outsourced accounting services, your provider needs these records to produce the most accurate closing data.

Additional elements of a strong month-end close process include:

- Reconciliations prepared to tie out AR, AP, Inventory and Fixed Asset subledgers to the balance sheet.

- A review of invoices for proper timelines – are they a monthly expense or longer term

- Review of fixed assets such as land, buildings, equipment, leasehold improvements and depreciation to determine if there are any changes

- Review of payroll, sales and other taxes to ensure timely payments and balances of local, state and federal tax obligations

- Review of expenses such as payroll, costs of goods sold, royalties, interest expense, utilities, repairs and maintenance, among others to be sure they are categorized properly

- Review for missing items that should be accrued for a more complete picture of income/expense items

Common Mistakes

Some common mistakes with the month-end close process include:

- Entering items on the P & L that should be taken to the balance sheet and spread over several months. These items might include prepaid subscriptions, licensing fees and insurance premiums, among other things. Generally, they are expenses that cover longer periods of time. On an annual basis, things balance out, but, on a monthly basis including these costs on the P & L skews the bottom line and presents an inaccurate financial picture.

- Similarly, if you buy equipment and enter the cost under repairs and maintenance on the P & L, it appears as if the company has higher operating expense than normal. These items have long-term value to the company and should be capitalized and then depreciated over their life. This allows the outsider to see improvements being made to increase the longevity of the company.

- Not adequately reviewing accounts payable and accounts receivable for old items is another common mistake. Any items that are beyond 90 days old need to be reviewed, researched and potentially written off. On the AP side, if you haven’t paid vendors, why is this happening? Do you have a cash flow problem? Do you need to reach out and establish a payment agreement with the vendors? Was there an issue with the product or service? Has it been resolved? This is a problem that needs to be addressed to ensure good working relationships with your vendors.

- It’s the same with the AR side. If you’re not reviewing AR regularly, you can have customers sliding out 60, 90 days and beyond. They may be in a crisis, and you may need to stop selling to them temporarily or propose a payment plan that is beneficial to both parties. This impacts you, the customer, and the bank. Communicate with that customer to find out what’s going on and if there is an issue. Are they dissatisfied with the product or service? This, again, needs to be addressed and rectified, not ignored. It could lead to bigger issues if it is not just this customer.

Identifying these issues in the month-end close is the key to taking care of them. This is where the value of outsourced accounting – utilizing current technology tools to generate real time data on your financial picture – proves its worth.

Responding to Problems

As a business owner, you need to rely on your financial team – your controller or CFO – to produce the data you need to make good business decisions.

- Ask them the hard questions. Do we have reconciliations for all balance sheet accounts? Can I see the reports? If your finance department can’t produce reconciliation reports they’re probably not reviewing them closely enough.

- If you find weaknesses in AR/AP, reach out and have conversations with customers and/or vendors. Take time to identify why the problems are happening and put in place steps to resolve issues.

- Look for trends. Ask for a trend report to see how expenses on P & L vary from month to month. If there are large spikes in certain accounts, such as repairs and maintenance, find out why. Normally, expenses are consistent from month to month. A large spike may indicate an item expensed on the P & L that should have been capitalized to the balance sheet.

- Be proactive in reviewing monthly financials and data rather than reactive to issues or problems that arise unexpectedly. It is a proven fact that anticipating concerns and planning accordingly is much more beneficial to the health of a company and it’s working relationships than ignoring until crisis mode and making knee-jerk decisions.

If you would like to strengthen your company’s month-end close process or discuss outsourced accounting services, please contact an Adams Brown advisor.